Jimmy Donaldson was 13 when he uploaded his first YouTube video. He was 26 when he became a billionaire. The trajectory between those two points reveals something more significant than viral fame. It exposes the mechanics of wealth creation in an economy that didn’t exist when his parents were his age.

MrBeast’s net worth in 2026 sits between $500 million and $1 billion, depending on how you value his private companies. The uncertainty itself tells you something important. Traditional celebrity wealth is salary-based and relatively transparent. Creator wealth is equity-based and deliberately opaque. Donaldson owns significant stakes in Feastables, his chocolate company currently valued at over $500 million. He holds licensing rights to Beast Burger, which generated $100 million in sales during its first year. His production company, Night Media’s portfolio company, employs over 100 people and produces content that reaches 400 million subscribers across platforms.

None of this was inevitable. Understanding how MrBeast built this fortune requires understanding what he did differently from every creator who came before him.

The Reinvestment Strategy That Changed Everything

Most YouTubers treat platform revenue as income. Donaldson treated it as seed capital.

His early videos cost nothing to produce. Gaming commentary, counting to 100,000, reading the dictionary. The content was unremarkable. What happened next wasn’t. Every dollar of ad revenue went back into production. A video that earned $10,000 funded a video that cost $15,000. That video earned $50,000, which funded a $75,000 production. The flywheel accelerated.

By 2020, individual MrBeast videos cost $1 million to produce. By 2023, production budgets exceeded $5 million per video. His Amazon Prime show, Beast Games, reportedly cost $100 million across its production run. The numbers sound reckless until you examine the returns.

A single MrBeast video generates between $3 million and $15 million in revenue across ad placements, sponsorships, and merchandise sales. His reinvestment rate, according to interviews, exceeds 100%. He spends more than he earns on content, funding the gap through his product companies and outside investment.

Traditional media executives would call this unsustainable. Donaldson calls it growth strategy. The distinction matters because he’s not trying to profit from content. He’s using content as customer acquisition for his real businesses.

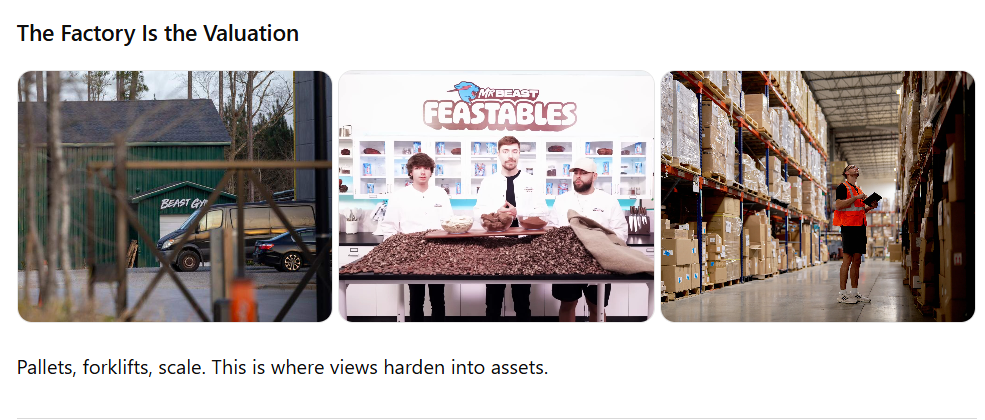

Feastables: The Real Wealth Engine

YouTube made MrBeast famous. Feastables is making him rich.

Launched in January 2022, Feastables started as a chocolate bar company. Within 18 months, it expanded into cookies, gummies, and snack foods. The company reached $200 million in annual revenue faster than any consumer packaged goods brand in history. Walmart, Target, and CVS all stock the products. International distribution spans 20 countries.

The economics reveal why creator-owned brands terrify traditional CPG companies. Feastables spends approximately zero dollars on paid advertising. Every MrBeast video functions as a commercial reaching 100 million viewers. The customer acquisition cost approaches zero. Traditional chocolate brands spend 15-25% of revenue on marketing. Feastables spends that money on product development and margin.

Venture capital firms valued Feastables at over $500 million in its last funding round. If Donaldson owns 50% of the company, a conservative estimate, that single asset represents $250 million of his net worth. Unlike YouTube revenue, which requires constant content creation, Feastables equity compounds whether he posts videos or not.

The Beast Burger Licensing Model

Beast Burger demonstrates a different wealth-building approach entirely.

Rather than building restaurants, Donaldson licensed his brand to existing commercial kitchens. Ghost kitchens, the delivery-only restaurants that proliferated during COVID, paid for the right to make Beast Burgers using his recipes and branding. The model required zero capital investment from Donaldson. He contributed brand and recipes. Partners contributed kitchens and labor.

At its peak, Beast Burger operated through 1,700 locations. First-year revenue exceeded $100 million. The licensing fees, typically 6-8% of sales, generated $6-8 million annually in essentially passive income. Quality control issues eventually led Donaldson to wind down the ghost kitchen model, but the experiment proved a principle. Creator distribution can monetize physical products without creator capital.

YouTube Revenue: The Loss Leader

Here’s the counterintuitive truth about MrBeast’s YouTube income. It probably loses money.

His main channel generates an estimated $50-80 million annually in ad revenue. Additional channels, including MrBeast Gaming, Beast Reacts, and international dubbed versions, contribute another $30-50 million. Total platform revenue likely reaches $100-130 million per year.

Production costs consume most of that. A single video budget of $5 million, multiplied by 50-60 videos annually across all channels, suggests production spending of $250-300 million. Sponsorship revenue covers some of the gap. His team size, estimated at 100+ employees with associated overhead, consumes more.

The math doesn’t work if you view YouTube as the business. It works perfectly if you view YouTube as marketing expense for Feastables, merchandise, and future ventures. Donaldson has said explicitly that he loses money on content. He’s buying attention at scale and converting it to product sales elsewhere.

This inversion, treating content as cost center rather than profit center, separates the wealthiest creators from the most-subscribed creators. They’re often different people.

The Philanthropy Question

MrBeast’s charitable giving complicates net worth calculations.

His philanthropy channel has funded cataract surgeries restoring sight to 1,000 people, built wells providing clean water to African villages, and given away houses, cars, and cash totaling tens of millions of dollars. Beast Philanthropy, structured as a separate entity, reportedly donates 100% of its revenue to charitable causes.

Critics question whether filmed charity constitutes genuine philanthropy or content production with tax benefits. The debate misses the structural innovation. Donaldson created a self-funding charitable vehicle where viewer attention directly converts to charitable giving. The model generates more donations than a traditional foundation could solicit.

Whether this generosity reduces his net worth depends on structure. If Beast Philanthropy donations come from company funds rather than personal assets, they’re business expenses reducing taxable income while generating content. If they come from personal wealth, they represent genuine net worth reduction.

The ambiguity is intentional. Creator finances, unlike public company finances, require no disclosure.

The Investment Portfolio Nobody Discusses

Beyond his own companies, Donaldson has become an active investor in the creator economy.

Night Capital, his venture arm, has invested in multiple creator-focused startups. Portfolio companies include tools for content production, merchandise fulfillment, and audience analytics. Each investment creates potential equity upside while providing services his own operation uses.

The venture model mirrors what tech founders discovered a decade ago. Build expertise in a vertical, invest in companies serving that vertical, benefit from information asymmetry and ecosystem effects. Donaldson knows which creator tools work because he uses them at scale. That knowledge informs investment decisions unavailable to traditional VCs.

Valuations of these investments remain private. If even a few succeed, they could add tens of millions to his net worth.

Real Estate and Hard Assets

Unlike many young wealthy individuals, Donaldson maintains a relatively modest real estate footprint.

His primary residence in Greenville, North Carolina, cost approximately $5 million. He owns production facilities and office space for his team. Total real estate holdings likely don’t exceed $20-30 million, conservative for someone with his liquid wealth.

This restraint may reflect either personal preference or strategic thinking. Real estate is illiquid. For someone reinvesting aggressively in growing businesses, tying capital in property reduces operational flexibility. The choice suggests Donaldson thinks like a growth-stage CEO rather than a wealth-preservation billionaire.

That orientation will likely shift as he ages. First-generation wealth typically moves toward real estate and diversified holdings over time. The Hamptons and similar markets should expect creator money within the next decade. Whether Donaldson specifically buys East End property remains speculative, but the demographic trend is clear.

Comparing MrBeast to Traditional Celebrity Wealth

Context illuminates what these numbers mean.

Leonardo DiCaprio, after 35 years of A-list Hollywood work, has a net worth of approximately $300 million. MrBeast exceeded that figure before turning 27. The comparison isn’t entirely fair. DiCaprio’s wealth is salary-based and relatively liquid. MrBeast’s is equity-based and largely illiquid until exit events.

Tom Cruise, the highest-paid movie star of his generation, has a net worth around $600 million after four decades of work. Dwayne Johnson, who combines film income with production company ownership and product deals, sits around $800 million. MrBeast competes with both while being young enough to be their son.

The comparison that matters most: Jerry Seinfeld’s net worth of $950 million came primarily from Seinfeld syndication rights, a passive income stream that continues decades after production ended. MrBeast is building similar passive income streams through product equity rather than content licensing. The wealth mechanics are converging even as the content formats diverge.

Risks to the Empire

No honest assessment ignores the vulnerabilities.

Platform dependency remains the existential risk. YouTube could change its algorithm, modify its revenue sharing, or face regulatory challenges that reduce creator earnings. TikTok’s uncertain American future demonstrates how quickly platform dynamics shift. Donaldson has diversified to Instagram, TikTok, and Amazon, but YouTube remains his primary distribution.

Audience fatigue presents another challenge. The spectacle escalation that built his audience requires ever-larger productions. At some point, the next video can’t be bigger than the last. How he navigates that ceiling will determine whether the empire expands or contracts.

Execution risk in his product companies is real. Feastables competes against Hershey, Mars, and Nestlé. These companies have century-long distribution relationships, manufacturing scale, and institutional knowledge that no startup can match. So far, distribution has overcome these disadvantages. Whether that continues through economic downturns or competitive responses remains uncertain.

Finally, key-person risk looms over everything. MrBeast is the brand. Unlike a company with institutional identity, his empire depends on his continued participation and creative direction. Any health issue, burnout, or pivot would immediately impact valuations across his portfolio.

What MrBeast’s Wealth Means for the Creator Economy

Individual success stories always risk overgeneralization. Not every creator can become a billionaire. Most won’t become millionaires. The structures Donaldson pioneered require scale that few achieve.

Still, his trajectory establishes possibilities that didn’t exist before. A teenager with no industry connections, no family wealth, and no geographic advantage built a billion-dollar enterprise through content and commerce integration. The path exists now. Others will follow it.

For family offices evaluating creator economy investments, MrBeast provides a template. Creator-led consumer brands with built-in distribution outperform traditional CPG launches on customer acquisition metrics. The investment thesis is proven, even if the specific opportunities require diligence.

For luxury brands considering creator partnerships, the lesson is structural. Sponsorship fees are the old model. Equity participation is the new expectation. Creators who understand their distribution value will negotiate accordingly.

For anyone watching new money patterns, MrBeast signals where wealth originates in the 2020s. The next generation of Hamptons buyers, charity gala hosts, and foundation founders will include people who built audiences before buildings. Understanding their wealth mechanics isn’t celebrity gossip. It’s market intelligence.

The Bottom Line on MrBeast’s Net Worth 2026

MrBeast’s net worth in 2026 ranges from $500 million to $1 billion, with the spread reflecting valuation uncertainty in private companies rather than disagreement about his success.

The figure matters less than the composition. Unlike celebrities whose net worth represents accumulated earnings, Donaldson’s wealth is primarily equity in growing companies. If Feastables continues its trajectory, his net worth could double within three years without any additional content creation. If the company falters, paper wealth could evaporate equally quickly.

What’s certain is the model. Content as customer acquisition. Products as profit center. Reinvestment over extraction. Equity over fees. These principles transformed a kid making YouTube videos in North Carolina into one of the wealthiest self-made individuals of his generation.

The next MrBeast is probably filming right now. The smart money is figuring out how to find them early.

Related Articles

- Logan Paul Net Worth 2026: PRIME, WWE, and the Multi-Platform Fortune

- PewDiePie Net Worth 2026: Gaming Legacy to Semi-Retirement Wealth

- The New Millionaires: How Digital Creators Build Generational Wealth

- Creator Wealth vs. Celebrity Wealth: Different Rules, Different Outcomes

Sources

- Forbes Creator Economy Coverage

- Bloomberg Business Analysis

- Financial Times on Influencer Marketing Market Size

- Company Press Releases and Funding Announcements

Author

Written by

Recent Posts

Midsommar A24 Cast Net Worth — The Daylight Horror That Turned Grief Into a Career Launchpad

ZOI NOMAD & TEN11 LOUNGE MARK ONE YEAR

Room A24 Cast Net Worth — The $6 Million Captivity Drama That Set Brie Larson Free

The Witch A24 Cast Net Worth — A $3.5 Million Puritan Nightmare That Created a Queen and a King

A24 Genre Stars Net Worth — The Terrifying Fortunes Behind Horror, Sci-Fi, and Oscar Gold

Categories

- Art

- Articles

- Beauty & Skincare

- Celebrities

- Celebrities|Movies

- Celebrities|The Chronicles

- Chronicles

- Entertainment|Culture

- Event Photos

- Events

- Fashion

- Fashion & Style

- Featured

- Food & Beverage

- Food, Spirits, Wine

- Hamptons

- Hamptons Celebrities

- Hamptons Celebrities|Celebrities|The Chronicles

- Health

- Health & Beauty

- Lifestyle

- Luxury Lifestyle

- Movies

- Movies|Culture

- Movies|Hamptons Lifestyle

- Press

- Profiles

- Real Estate

- Technology

- The Chronicles

- Travel

- Uncategorized

- Weddings