Carl Icahn net worth peaked at approximately $25 billion in early 2023. At that point, he ranked among the top sixty richest people on earth. He was the wealthiest man on Lily Pond Lane. By May 2, 2023, $10 billion disappeared from that figure in a single trading session. That was the day Hindenburg Research published its short-seller attack on Icahn Enterprises. By early 2026, with Icahn Enterprises LP (IEP) trading at roughly $8 per unit against a former peak above $100, most estimates place his fortune near $5 billion. The collapse is one of the largest single-decade personal wealth destructions in modern financial history. Notably, Icahn does not appear to be leaving. He purchased another 30 million IEP shares in Q4 2025, reinforcing a position that now represents nearly 50% of his reported investment portfolio.

Notably, the man who invented the playbook every activist investor in this series studied is the one who lost the most by it.

The Room Before the Room

Carl Celian Icahn was born on February 16, 1936, in Brooklyn. His family later settled in Far Rockaway, Queens. His father Michael was a cantor and later substitute teacher; his mother Bella taught public school. The neighborhood was working class. Money was not taken for granted. At Far Rockaway High School, Icahn was a strong enough student to gain admission to Princeton, where he studied philosophy and graduated in 1957. Notably, the philosophy background matters more than it initially appears. Icahn has consistently framed his investment strategy as a logical exercise. He identifies systems operating below their rational potential and forces correction.

After Princeton, he enrolled at New York University’s School of Medicine. Subsequently, he dropped out after two years, joined the Army Reserves, and entered Wall Street in 1961 as a stockbroker at Dreyfus Corporation. Additionally, he worked as an options manager at Tessel, Patrick & Co. and later at Gruntal & Co. By 1968, Icahn had accumulated $150,000 of his own savings. His uncle, M. Elliot Schnall, invested another $400,000. Together, they purchased a seat on the New York Stock Exchange. Icahn & Co. was founded that year, focused on risk arbitrage and options trading. The company was small. His ambition was not.

The First Raid: Tappan, 1978

Ultimately, Icahn’s first hostile takeover attempt came in 1978. He acquired a controlling stake in Tappan, an appliance manufacturer, and forced its sale to Electrolux. The move doubled his investment. Consequently, the method was established. Identify a company trading below what a forced transaction would unlock. Accumulate enough shares for leverage. Apply pressure publicly. Collect the premium. Moreover, what distinguished Icahn from the gentlemanly M&A world of the 1970s was his willingness to use that pressure regardless of whether management wanted to sell. He was not invited into those boardrooms. He kicked the door.

The Belief System — Corporate Raiding as Governance Theory, Shown Through Two Campaigns

Icahn’s core argument is simple: entrenched management destroys shareholder value. Outside pressure from a credible, large stakeholder is the most efficient corrective available. He developed and applied this thesis across fifty years and hundreds of companies. In practice, that meant accumulating enough stock to become impossible to ignore. He demanded board seats and operational changes. Either those changes happened, or a transaction was triggered that realized value anyway. Unlike the era’s other corporate raiders, Icahn rarely needed Milken’s junk bond machine to execute. He built his war chest from the campaigns themselves, compounding position by position across decades.

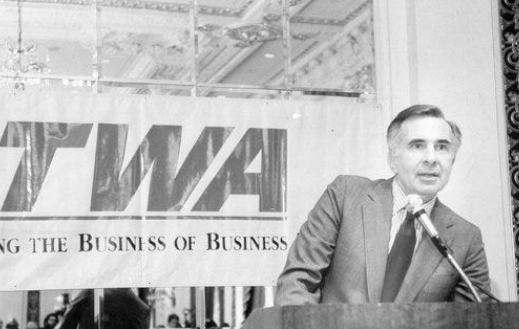

TWA: The Campaign That Made and Cost Him

Trans World Airlines was Icahn’s most consequential and most complicated campaign. In the mid-1980s, he accumulated a 50% stake, then completed a full leveraged buyout of the airline. Subsequently, he sold TWA’s prized London routes to American Airlines for $445 million. The transaction personally enriched Icahn. Meanwhile, it sent TWA into $540 million worth of debt. Critics labeled it textbook asset stripping. Icahn’s defenders argued he had identified a structurally broken airline and extracted the only real value it contained. Both readings are available. Furthermore, the TWA campaign established a pattern that defined the public’s ambivalence toward Icahn for four decades. Shareholder returns and collateral damage ran simultaneously, inextricably, on the same ledger.

Apple, Dell, and the Modern Era

By the 2010s, Icahn had pivoted from hostile raids to large-stake activist campaigns at some of America’s most significant companies. In 2013, he purchased nearly $2 billion in Apple stock. He publicly pressured Tim Cook to accelerate share buybacks. The campaign generated enormous media attention and, ultimately, Apple’s compliance. He also bought nearly $2 billion in Dell stock in 2013 as the company prepared to go private. He challenged Michael Dell’s buyout valuation. Ultimately, he conceded to the transaction. Additionally, Icahn ran major campaigns at Motorola, Biogen, eBay, Xerox, Occidental Petroleum, and Southwest Gas Holdings. His most famous defensive battle was the multi-year public war with Bill Ackman over Herbalife. Ackman was short; Icahn was long. Icahn ultimately sold his stake at a profit. Rosenstein ranked himself alongside Icahn. Ackman measured his career against Icahn. That is a particular kind of market gravity.

The Timeline: From a $150,000 Stake to the IEP Collapse

| Period | What Happened | Net Worth / Asset Marker |

|---|---|---|

| 1936–1968 | Born Brooklyn, raised Queens. Princeton BA philosophy (1957). NYU Medical School dropout. Army Reserves. Stockbroker at Dreyfus (1961). Options manager at Tessel and Gruntal. 1968: purchases NYSE seat with $150K personal + $400K from uncle. Founds Icahn & Co., risk arbitrage and options. | — |

| 1978–1984 | First hostile campaign: Tappan Company, forces sale to Electrolux, doubles investment. Campaigns at ACF Industries (sold stake to Phillips Petroleum for $50M profit). Reputation as “corporate raider” established. Acquires significant stake in Texaco. Accumulates war chest through compounding campaigns. | ~$300M+ |

| 1985–1993 | TWA: acquires 50% stake, completes LBO. Sells London routes to American Airlines for $445M (TWA absorbs $540M in debt). Acquires Marvel Comics (1989) — declares bankruptcy 1996, sells 1997. Acquires five bankrupt S&Ls; renamed First Gibraltar Bank. Sells to Bank of America for $1B (1993). Bloomberg ranks him richest person in NYC (March 2012) at $20B. | ~$5B–$10B |

The Modern Activist Era: 2000–2023 |

||

| 2000–2022 | Establishes Icahn Enterprises LP (IEP) as primary public vehicle. IEP stock peaks above $100/unit. Runs major campaigns: Apple ($2B position, 2013), Dell ($2B, 2013), Motorola, Biogen, eBay, Herbalife (vs. Ackman), Xerox, Occidental Petroleum, Southwest Gas. Fontainebleau Las Vegas acquired for ~$150M (2010), sold for $600M (2017). Net worth peaks at ~$25B February 2023. | Peak: ~$25B (Feb 2023) |

| May 2023 | Hindenburg Research publishes short report: IEP overvalued 75%+, “Ponzi-like” dividend structure, margin loans undisclosed. IEP falls 20% in one day, erasing $3.1B. Margin loan disclosure removes another $7.3B from Bloomberg calculation. Net worth drops 41% to ~$14.6B in one session. US Attorney for Southern District of NY contacts IEP. SEC enforcement division contacts IEP in August 2023. | $25B → $14.6B in one day |

| Aug 2023–2026 | IEP slashes dividend from $2 to $1/unit (August 2023), then to $0.50/unit. IEP stock falls from ~$50 to ~$8 (March 2026) — down 88% from peak, lowest since early 1990s. IEP indicative NAV ~$3.2B (Dec 2025). FY2025: revenues $9.7B, net loss $299M. Icahn purchases additional 30.5M IEP units in Q4 2025 (~$245M); now holds 549M units (~86% of IEP). IEP market cap ~$4.4B. Net worth est. ~$5B. | ~$5B (est. early 2026) |

The Hamptons Chapter: Lily Pond Lane and the Palace That Stayed

Among the East End’s financial elite, Carl Icahn’s Lily Pond Lane estate occupies a category of its own. The seven-acre compound in East Hampton consists of three separate houses and two tennis courts. Gardens on the property have been described by visitors as roughly the size of a football field. Neighbors on the lane have included Jon Bon Jovi, Steven Spielberg, and Martha Stewart. Area brokers have estimated the estate’s value at $40 million to $50 million. That places it among the most valuable compound properties on one of the Hamptons’ most storied private streets. The main residence carries an antique French architectural style — white-painted, palace-scale, with tennis courts flanking the grounds.

Notably, Icahn’s Lily Pond Lane presence predates the second-generation hedge fund wave that reshaped East Hampton pricing in the 2010s and 2020s. Moreover, Barry Rosenstein paid $147 million for Further Lane and built a compound for the press to document. Ronald Perelman’s Georgica Pond parties defined a social era. By contrast, Icahn’s East Hampton estate operates on his characteristic terms: present, permanent, and largely unannounced. He does not host the party of the summer. He is simply there, decade after decade, on the lane where the serious money summers.

The Lily Pond Lane Address Book

Lily Pond Lane occupies a specific register in Hamptons geography. It is less transactional than Further Lane, less storied than Meadow Lane. However, it draws figures who have operated at the top of their respective industries for decades rather than years. Icahn has owned his compound through multiple market cycles, four decades of activist campaigns, and the most public financial reversal of his career. Furthermore, the compound has not appeared on the market during the IEP crisis years. Whatever the net worth figure reads in early 2026, the Lily Pond Lane estate is not part of the liquidation equation — at least not yet.

Carl Icahn Net Worth: What He Actually Built — and What IEP Became

Carl Icahn net worth, at its peak of approximately $25 billion, derived almost entirely from his 85% to 86% stake in Icahn Enterprises LP. IEP is a publicly traded limited partnership spanning energy, automotive, food packaging, real estate, home fashion, and pharmaceuticals. It served as the primary vehicle for virtually all of Icahn’s investments. At IEP’s peak trading price above $100 per unit, that stake was worth roughly $20 billion on its own. The company also paid a 15.8% dividend yield that attracted retail investors — the highest yield of any U.S. large cap company at the time — which Hindenburg identified as both the most alluring and most structurally questionable feature of the IEP investment thesis.

Additionally, Icahn’s personal investment funds — in which he and son Brett Icahn were the only investors — held approximately $4.9 billion at the end of 2022. The IEP structure relied on Icahn taking his own dividend in additional units rather than cash. This reduced the cash outlay required to sustain the payout for other unitholders. Hindenburg outlined this structure; subsequent events confirmed it. Consequently, when IEP’s stock fell, the margin loans Icahn had taken against his position were disclosed. The entire architecture of how his net worth had been calculated changed in a single afternoon.

The Current State of IEP

Consequently, by early 2026, IEP trades at approximately $8 per unit — down roughly 88% from its pre-Hindenburg levels, and at its lowest point since the early 1990s. FY2025 revenues reached $9.7 billion across seven operating segments, with adjusted EBITDA of $338 million attributable to IEP and a net loss of $299 million. Indicative net asset value at year-end 2025 was approximately $3.2 billion, down from $3.8 billion in Q3 2025. Icahn holds approximately 549 million IEP units, representing 86% of the partnership. At $8/unit, that stake is worth roughly $4.4 billion before accounting for the margin loans secured against it. The company maintains approximately $2.7 billion of liquidity in its investment segment. IEP’s most recent analyst rating is a Sell at an $8.00 price target. Icahn, 90 years old in February 2026, continues as controlling shareholder and recently added to his position.

Public Reputation vs. What the Room Goes Quiet About

The established Icahn narrative is this: he is the original activist investor. He made hostile takeovers legally mainstream. He ran the first large-scale campaign at a Fortune 500 company before anyone else had a playbook. Furthermore, he spent five decades extracting returns from a market that rewarded his particular combination of aggression, patience, and willingness to be publicly wrong while accumulating. His Princeton philosophy degree was not incidental. He understood the logic of entrenched management’s irrationality better than the management consultants who served them. Furthermore, every activist investor in this series — Rosenstein, Black, Tepper, Griffin — learned from Icahn’s framework, whether they acknowledge it or not.

The TWA Ledger and the IEP Mirror

Inside the room, however, two accounts run alongside that legacy. First, the TWA precedent established a question that has never fully resolved itself. Does the shareholder value thesis account for the non-shareholder costs of how that value is extracted? The London routes returned $445 million to Icahn. They sent TWA $540 million into debt. Workers, pensioners, and the airline’s long-term customers absorbed costs that do not appear in the return calculation. Second, the IEP structure that Hindenburg exposed in 2023 raised a more direct question. The man who built a fifty-year career accusing corporate managements of financial opacity had constructed a vehicle with undisclosed margin loans. Additionally, the dividend structure depended on his own reinvestment cycle. Asset valuations that three subsequent quarterly disclosures proved overstated completed the picture. The irony is too precise for anyone close to the situation to avoid.

The Hindenburg Defense and What It Revealed

Icahn’s response to Hindenburg was characteristically defiant. He called the report “self-serving” and compared Nate Anderson’s firm to “Blitzkrieg Research.” Subsequently, IEP cut its dividend in half. Then it cut it again. The SEC enforcement division contacted the company in August. Shortly after, the US Attorney’s Office for the Southern District of New York made its own inquiry. None of those events produced charges or findings against Icahn personally. IEP continues operating across seven business segments with $12.2 billion in assets as of December 2025. Ultimately, however, the sequence confirmed the Hindenburg thesis on the dividend’s sustainability more thoroughly than any short report could have managed on its own.

Contribution: Choate, the Children’s Rescue Fund, and a $20 Billion Pledge

Carl Icahn’s philanthropy operates at a scale that receives far less coverage than his investment campaigns. He signed the Giving Pledge — committing to donate the majority of his fortune to charitable causes — and has publicly stated a $20 billion giving target over his lifetime. Furthermore, his most visible charitable infrastructure runs through New York City. Icahn House East and Icahn House West are homeless shelters serving unmarried pregnant women and single mothers with children. Both are funded by Icahn’s Children’s Rescue Fund. Additionally, the Carl C. Icahn Center for Science at Choate Rosemary Hall endows the Icahn Scholar Program, providing ten students annually with full tuition, room and board, books, and supplies across four years. The endowment runs approximately $400,000 per year.

Moreover, Icahn has made substantial gifts to Mount Sinai Hospital in New York, where the Icahn School of Medicine bears his name following a transformative donation. He has also funded cancer research, pediatric medicine, and various educational initiatives in New York City. Given the Giving Pledge commitment and the infrastructure already built, Icahn’s charitable giving is one of the more significant legacy dimensions of any figure in this series. It is also among the most underreported.

The Icahn School of Medicine

The Mount Sinai naming is the centerpiece. In 2013, the Icahn School of Medicine at Mount Sinai formalized a major gift relationship. Icahn’s name now appears on one of New York’s leading academic medical institutions. Consequently, that outcome carries a particular resonance — the NYU Medical School dropout now names a New York medical school. Consequently, the biographical arc from Queens medical school dropout to named benefactor of a New York medical school carries a specific texture that the financial biography alone cannot convey.

The East End Verdict on Carl Icahn Net Worth

Carl Icahn net worth is the ledger of the man who, more than anyone else in this series, built the conceptual infrastructure that everyone else inherited. Leon Black learned distressed debt from Drexel. Barry Rosenstein built JANA on an Asher Edelman apprenticeship — Edelman who came from Icahn’s era. Ken Griffin built a market-neutral machine. Icahn built the original argument: public companies are systematically mismanaged. A determined outside shareholder with enough patience and capital can force the market to acknowledge what management refuses to.

On Lily Pond Lane, the seven-acre compound still stands — three houses, two tennis courts, garden the size of a football field. Icahn has held it through the TWA controversy, through the Herbalife war, through the peak at $25 billion, and through the Hindenburg correction to $5 billion. Furthermore, at 90 years old in 2026, he spent $245 million in Q4 2025 buying more of the company the short sellers say is broken. That is either the conviction of a man who has been right fifty times before. Alternatively, it is the last reflex of a legacy that can no longer separate pride from position sizing. Social Life Magazine has documented the East End’s power corridor for 23 years. No figure in the Hamptons financial ecosystem has a longer tenure, a larger founding influence, or a more complicated current chapter than the man on Lily Pond Lane.

The Number That Defines the Record

Among all the figures in this series, Icahn alone has a campaign that a federal court, a generation of airline historians, and a US Senate subcommittee have examined for its collateral costs. That campaign is TWA. He alone built a publicly traded vehicle that became the primary mechanism for his personal net worth and then watched it fall 88% in three years. He alone, at 90, added $245 million to that position in Q4 2025. The $5 billion is not the number that defines the record. The number that defines it is 1968. That year, a Queens kid and his uncle’s $400,000 bought a seat on the New York Stock Exchange. Consequently, the framework every activist investor in this series subsequently used was built from that single transaction.

Want Social Life to document your East End story? The people in this series built their positions before anyone was watching. Contact Social Life Magazine — 23 years on the East End.

The Hamptons deal table, live: Polo Hamptons — sponsorships, VIP access, and brand activations where the real decisions get made.

The Hamptons insider list: Subscribe to Social Life Magazine — print and digital.

Support independent Hamptons journalism: Donate $5

Related Reading:

Barry Rosenstein Net Worth: The $147M Further Lane Bet

Leon Black Net Worth: Apollo’s $13B Shadow on Meadow Lane

Ken Griffin Net Worth: Citadel’s $49B Meadow Lane Titan

Ronald Perelman Net Worth: The Creeks and a $19B Fall

Henry Kravis Net Worth: KKR’s $12B Meadow Lane Patriarch

Hamptons Hedge Fund Billionaires: The Complete Net Worth Guide

Carl Icahn net worth data sourced from Bloomberg Billionaires Index, Forbes, SEC 13F filings, and Icahn Enterprises LP public filings. IEP financial data from company earnings releases and investor presentations. Real estate details from public reporting. Social Life Magazine is an independent publication and has no affiliation with Carl Icahn or Icahn Enterprises LP.

Author

Written by

Recent Posts

7 Mindful Meal Prep Tips for Stop Food Waste Day

Rebecca Ferguson Net Worth: The Advantage of Not Being the Lead

What Makes a Dinner Party Truly Unforgettable (Hint: It’s Not the Food)

Tips for Managing Grease and Oil in Everyday Dishwashing

Austin Butler Net Worth: The Method Actor in a Post-Method World

Categories

- Art

- Articles

- Beauty & Skincare

- Celebrities

- Celebrities|Entertainment

- Celebrities|Television

- Celebrities|The Chronicles

- celebrities|the-archive

- Chronicles

- Entertainment|Culture

- Event Photos

- Events

- Fashion

- Fashion & Style

- Featured

- Food & Beverage

- Food, Spirits, Wine

- Hamptons

- Hamptons Celebrities

- Hamptons Celebrities|Celebrities|The Chronicles

- Health

- Health & Beauty

- Lifestyle

- Luxury Lifestyle

- Movies

- Press

- Profiles

- Real Estate

- Technology

- The Chronicles

- Travel

- Uncategorized

- Weddings