The thing nobody says at the polo match is that three of the eight men profiled here have compounds within a quarter mile of each other on Meadow Lane. They have sued each other’s portfolio companies, testified against each other’s business partners, and competed for the same institutional capital for decades. On the East End, they are neighbors. The polo match proceeds accordingly.

Hamptons hedge fund billionaires net worth, taken across these eight men, totals somewhere north of $120 billion — a figure that moves daily with public markets but has remained, through multiple financial crises and at least two personal reckonings that went very public, among the highest concentrations of private capital per square mile anywhere on earth. Social Life Magazine has covered this corridor for 23 years. What follows is the definitive accounting: who built what, what it actually cost, and what the three miles between Sagaponack and East Hampton finally say about the people who chose it.

Hamptons Hedge Fund Billionaires Net Worth: At a Glance

| Name | Est. Net Worth | Hamptons Address | Primary Vehicle | Defining Move |

|---|---|---|---|---|

| Ken Griffin | ~$49.6B | Meadow Lane, Southampton | Citadel / Citadel Securities | $1.15B Meadow Lane compound; $63B AUM |

| Carl Icahn | ~$5B | Lily Pond Lane, East Hampton | Icahn Enterprises (IEP) | Invented modern activist investing; IEP down 88% post-Hindenburg |

| David Tepper | ~$20B | Further Lane, East Hampton | Appaloosa Management | Greatest single trade in hedge fund history; demolished Goldman partner’s mansion |

| Leon Black | ~$13B | Meadow Lane, Southampton | Apollo Global Management | $908B AUM; $120M for The Scream; Epstein fallout ends Apollo tenure |

| Henry Kravis | ~$12.5B | Meadow Lane, Southampton | KKR | Co-invented leveraged buyout; $744B KKR AUM; 20+ years on Meadow Lane |

| George Soros | ~$7.2B personal / ~$40B lifetime | Southampton | Open Society Foundations | Broke the Bank of England 1992; donated $32B; most philanthropic fortune in series |

| Ronald Perelman | ~$3–4B | The Creeks, Georgica Pond, East Hampton | MacAndrews & Forbes | Peaked $19B; Revlon hostile takeover rewrote M&A law; The Creeks sold 2022 for $84.5M |

| Barry Rosenstein | ~$1.5B | Further Lane, East Hampton | JANA Partners | Paid $147M for Further Lane — most expensive U.S. residential sale at the time |

Ken Griffin: The Man Who Didn’t Buy a House. He Bought a Position.

Ken Griffin started Citadel in 1990 with $265,000 raised from his Harvard dorm room. He now manages $63 billion in hedge fund assets and runs Citadel Securities, the market-making operation that processes roughly 25% of all U.S. equities volume daily. Notably, that last number is worth sitting with: one firm, processing one in four American equity trades, built by a man who was 22 years old and technically a student when he started it.

His Meadow Lane assemblage cost more than $1.15 billion across multiple adjacent parcels — the most expensive private residential assemblage in American history. Furthermore, Griffin relocated Citadel’s headquarters from Chicago to Miami in 2022. His primary East Coast fixed point is now the Southampton compound, not an office tower. By contrast, most billionaires treat real estate as a reflection of their net worth. Griffin treats it as an extension of his infrastructure. The distinction matters more than it sounds.

He is the wealthiest person on the East End by a figure that rounds to $30 billion more than the next name on this list. Consequently, the Meadow Lane compound isn’t a trophy. It’s a statement about what systematic, quantitative dominance looks like when it fully matures. Full profile: Ken Griffin Net Worth.

David Tepper: The Goldman Rejection Was the Real Trade

In 1993, Goldman Sachs declined to make David Tepper a partner. He left and founded Appaloosa Management. Sixteen years later, he returned $7 billion to himself in a single calendar year by buying distressed bank debt — Bank of America, Citigroup, the institutions the market had written off as finished — for cents on the dollar, then holding through the government bailout. Appaloosa returned 132% in 2009. That is the greatest single-year return in hedge fund history.

However, the Sagaponack property tells a more specific story. Tepper paid $43.5 million for an oceanfront mansion that had belonged to a former Goldman partner. He then demolished it. He built a replacement twice the size on the same footprint. The trade that made him $7 billion was financial. Additionally, the demolition was personal. He has not, to public knowledge, elaborated on the distinction.

Tepper now owns the Carolina Panthers and Charlotte FC. His $20 billion fortune extends well beyond distressed debt into sports, real estate, and the particular satisfaction, apparently, of building large things on land that used to belong to someone else. Full profile: David Tepper Net Worth.

George Soros: Forbes Shows $7.2 Billion. The Actual Number Is $40 Billion.

Forbes lists George Soros at approximately $7.2 billion. That number is technically accurate and practically misleading. Over his lifetime, Soros transferred more than $32 billion to Open Society Foundations — the largest philanthropic transfer in history by a living individual. The wealth didn’t disappear. He moved it. The Forbes Real-Time Billionaires list measures what he kept, not what he built.

The fortune behind those donations came from Quantum Fund and, most famously, the 1992 trade against the British pound. On Black Wednesday, Soros shorted sterling against the European Exchange Rate Mechanism and netted approximately $1 billion in a single trading session. The Bank of England withdrew from the ERM. Notably, a private citizen had broken a central bank, and the mechanism that broke it was a thesis about political will, not financial modeling.

His Southampton estate has been part of the East End landscape for decades — present, low-profile, consistent with a philosophy that has always valued strategic position over display. Furthermore, he is simultaneously the most misunderstood figure in this series and the one whose financial philosophy is most coherent across the full arc of his life. The $7.2 billion is the remainder. The $32 billion was the point. Full profile: George Soros Net Worth.

Leon Black: The Institution Survived. The Question Is What That Means.

Leon Black built Apollo Global Management into a $908 billion alternative asset institution across four decades of distressed debt, leveraged buyouts, and institutional fundraising. His personal net worth of approximately $13 billion reflects ownership stakes and carried interest accumulated over that period. Meanwhile, his art collection at its peak approached $1 billion in value, anchored by the Edvard Munch Scream, purchased at auction for $120 million in 2012 — a record at the time.

In 2021, Black stepped down as Apollo’s CEO following disclosures about $158 million in payments to Jeffrey Epstein for estate planning and tax advice. The institution he built continues. Consequently, Apollo now manages assets that make Black’s personal net worth look like a rounding error in its own quarterly report. That is either a measure of what he created or a specific kind of irony, depending on how you want to read it.

The Meadow Lane compound sits adjacent to Griffin’s assemblage. The address communicates peer-group standing that no press release manufactures. Additionally, it endures as the most visible fixed asset of a legacy the public record has made considerably more complicated than the $908 billion number suggests. Full profile: Leon Black Net Worth.

Henry Kravis: The Deal That Made Him Famous Almost Broke Him

Henry Kravis, George Roberts, and Jerome Kohlberg founded KKR in 1976 without an institutional framework for what they were proposing to do. No established mechanism existed for buying a public company with borrowed money, reorganizing it, and selling at a premium. Notably, KKR built that framework. Every private equity firm that followed built on the foundation KKR established before any of them existed.

Today, KKR manages approximately $744 billion in assets and generates roughly $1 billion in fee-related earnings each quarter, according to Bloomberg. Kravis’s personal fortune of approximately $12.5 billion derives primarily from his approximately 76 million KKR units. However, the 1988 RJR Nabisco transaction — the $31.4 billion deal immortalized in Barbarians at the Gate — generated a net loss for KKR. The deal made Kravis the most recognized face of an era. It also lost money. That detail rarely surfaces in the profile pieces.

On Meadow Lane, Kravis has held a six-bedroom oceanfront estate for more than 20 years without apparent need to upgrade, expand, or signal anything beyond continued presence. By contrast with Griffin’s assemblage and Black’s collection, that restraint is itself a statement. Full profile: Henry Kravis Net Worth.

Ronald Perelman: $19 Billion, Then $3 Billion, Then the Fire

For more than a decade, The Creeks — Perelman’s 57-acre Georgica Pond estate, a 40-room Mediterranean villa built in 1899 — hosted the Apollo in the Hamptons fundraiser. McCartney performed there. So did Sting, Bon Jovi, Timberlake, and Pharrell. Perelman’s net worth peaked at approximately $19 billion in 2018. Three years later it had contracted to roughly $3 billion, which is not a rounding error. That is a different life.

Revlon, burdened by $3 billion in debt from a 2016 acquisition and damaged by COVID supply chain exposure, filed Chapter 11 in June 2022. Perelman liquidated approximately $1 billion in art. Additionally, a $410 million insurance dispute over five artworks lost in a 2018 attic fire went to trial in June 2025, with Ken Griffin called as a witness. The Creeks, listed as a pocket listing at $180 million, was not sold. Instead, Perelman sold his Lily Pond Lane oceanfront property for $84.5 million in January 2022.

The Creeks era does not exist anymore. Furthermore, what makes Perelman’s arc the most instructive in this series isn’t the fall itself. It’s that the parties were real, the art was real, and the leverage was real all at the same time, for years, in the same 57 acres. Full profile: Ronald Perelman Net Worth.

Barry Rosenstein: The House Held. The Fund Didn’t.

In May 2014, Barry Rosenstein paid $147 million for an 18-acre oceanfront compound at 60 Further Lane in East Hampton — the most expensive residential sale in United States history at the time. He then demolished the existing residence and commissioned Rick Cook of CookFox to design a 16,300-square-foot replacement with an 82-foot lap pool and a terrace the project documentation formally designates “Barry’s Terrace.” No Hamptons residential transaction has exceeded $147 million since.

Rosenstein founded JANA Partners in 2001 with $35 million and built it into an $11 billion activist platform. His signature campaign was Whole Foods: he disclosed an 8.8% stake in April 2017, pressed for board changes, and by June 2017 had sold his position to Amazon for approximately $300 million in profit. Notably, JANA’s AUM has contracted to approximately $2 billion since that peak. The fund shrank. The house appreciated. The property record stands.

By contrast with Tepper’s demolition story, Rosenstein’s Further Lane narrative has no visible personal subtext. He saw an asset worth $147 million and paid it. Furthermore, twelve years of subsequent market data have not contradicted that judgment. Full profile: Barry Rosenstein Net Worth.

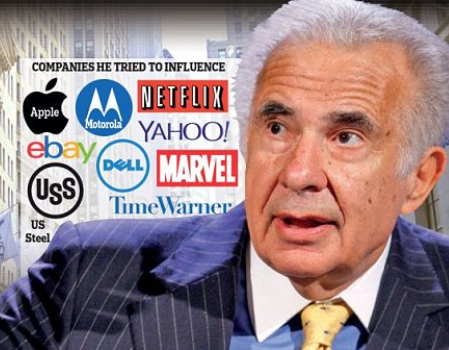

Carl Icahn: He Invented the Playbook. Then He Lost to It.

Carl Icahn’s core thesis, developed in the 1970s and applied at hundreds of companies across five decades, is that entrenched management destroys shareholder value. A determined outside shareholder with enough patience and capital can force the market to acknowledge what management refuses to. That thesis made him a billionaire. At his peak in early 2023, it had made him worth approximately $25 billion.

On May 2, 2023, Hindenburg Research published a short report on Icahn Enterprises LP. Ten billion dollars disappeared in one trading session. By early 2026, IEP trades at approximately $8 per unit — down 88% from pre-Hindenburg levels. Hindenburg’s argument was, essentially, that the structure of IEP had become precisely the kind of value-destructive mechanism Icahn had spent his career targeting. Consequently, the man who taught every activist investor in this series lost the most by the playbook he authored.

His net worth currently sits near $5 billion. His seven-acre Lily Pond Lane compound — three houses, two tennis courts — has not moved. Additionally, in Q4 2025, at age 89, Icahn purchased another 30 million IEP shares. Whether that is conviction or refusal is a question worth sitting with for a moment before moving on. Full profile: Carl Icahn Net Worth.

What Eight Fortunes Built on the Same Three Miles

The Geography of the Fortune

Hamptons hedge fund billionaires net worth, taken as a collective, reveals a specific geography of American capital. Meadow Lane in Southampton holds three of the eight: Griffin, Black, and Kravis. Further Lane in East Hampton holds Tepper and Rosenstein. Lily Pond Lane holds Icahn. The Creeks occupies Georgica Pond. Soros anchors Southampton from a quieter register. These are not random residential choices. Each address communicates a precise social position within a peer group that measures standing by oceanfront frontage, lot size, and the specific lane rather than the zip code.

Moreover, the eight fortunes divide cleanly along generational lines. Icahn, Kravis, Perelman, and Soros built their primary positions in the 1970s and 1980s — the era of hostile takeovers, junk bonds, leveraged buyouts, and macro currency bets. Meanwhile, Tepper, Black, and Rosenstein built in the 1990s and 2000s, when the institutional infrastructure those earlier figures created had matured into the alternative asset industry. Griffin represents the third generation: quantitative, market-neutral, systemized, operating at a scale that makes the earlier generations look boutique by comparison. Notably, each generation built on the ruins of what the previous one had been criticized for.

The Declining Fortunes and the Lesson They Encode

The series reveals a clear pattern. Earlier-generation fortunes have contracted significantly while the quantitative third-generation position continues to compound. Perelman fell from $19 billion to roughly $3 billion. Icahn fell from $25 billion to $5 billion. Soros transferred $32 billion to Open Society. Rosenstein’s JANA contracted from $11 billion AUM to $2 billion. By contrast, Griffin’s Citadel grew from a dorm-room concept to a $63 billion hedge fund generating consistent double-digit returns across market cycles, according to Bloomberg Billionaires Index data.

Ultimately, the Hamptons geography encodes a lesson the financial press rarely states directly: the method outlasts the ambition. The men who systematized earliest held the most. The men who held longest to a single concentrated philosophy held the least. Furthermore, the real estate absorbed all of it without comment.

The Addresses as a Competitive Score

The real estate decisions in this group function as a secondary ledger — a record of conviction, timing, and ego that runs parallel to the financial returns. Griffin paid over $1 billion for Meadow Lane, the most expensive residential assemblage in American history. Rosenstein paid $147 million for Further Lane at a price the market called excessive and that still represents the single highest Hamptons residential transaction ever recorded. Kravis has held Meadow Lane for 20 years without apparent need to upgrade or expand. Icahn holds Lily Pond Lane through the worst financial reversal of his career. Notably, these are not properties bought for investment return. They are positions held because leaving would mean something, and none of these men have decided to mean that yet.

Why the East End and Not Somewhere Easier

The question worth asking is why the South Fork specifically — rather than Greenwich, Palm Beach, or the Palisades — became the primary summer residence for this concentration of hedge fund and private equity capital. The answer has several components. First, geographic constraint: Further Lane, Meadow Lane, and Lily Pond Lane cannot be expanded. The oceanfront is physically finite. Consequently, the scarcity that drives luxury real estate pricing everywhere operates here with unusual purity.

Additionally, the social network effect matters considerably. Kravis chose Meadow Lane, and it drew Black and eventually Griffin. Perelman anchored Georgica Pond, pulling a generation of entertainment and finance money that reshaped East Hampton’s summer social calendar. Rosenstein chose Further Lane, buying into the Tepper corridor. Furthermore, these addresses are not independent choices — they are cluster investments in a specific social infrastructure, made by men who understand cluster dynamics better than anyone.

The Hamptons also functions as neutral territory for a competitive industry. These eight men have fought each other publicly — Icahn and Ackman over Herbalife, Perelman and various counterparties over Revlon’s debt structure, Black and his Apollo board over the Epstein disclosure. However, on the East End, they are simply neighbors. The social contract of the Hamptons summer — the polo matches, the charity dinners, the benefit galas — provides a framework for maintaining relationships across competitive lines. Furthermore, Social Life Magazine has documented that dynamic since 2001. Our Polo Hamptons events operate at precisely this intersection: competitive finance, shared geography, and the specific social grammar of the East End summer.

The East End Verdict on Hamptons Hedge Fund Billionaires Net Worth

The aggregate number — $120 billion, give or take a market session — tells only part of the story. The more accurate measure is what each of these eight men did with the framework they inherited or invented. Icahn built the concept first, then watched it come back around. Kravis and Perelman commercialized it into private equity, with varying results. Soros weaponized it at a macro scale no one had attempted before or since, then gave most of the proceeds away. Tepper took the distressed-debt logic to its theoretical maximum in 2009 and used some of the proceeds to demolish a house that deserved it. Black scaled the institutional infrastructure to $908 billion before the institution decided it could continue without him. Rosenstein applied activist methodology to underperforming consumer brands and bought a $147 million house that has outlasted the fund.

The East End as Final Answer

Meanwhile, Griffin rebuilt the entire premise from scratch — quantitative, systematic, divorced from the relationship-based deal flow that defined the earlier generations, operating at a scale that makes every other name in this piece look like a prototype. Hamptons hedge fund billionaires net worth, across this series, is ultimately a record of eight different answers to the same question: what is an asset worth, who decides, and how much force does it take to make the market agree? The East End is where those eight answers rest for the summer. Three miles of oceanfront, eight compounds, fifty years of American capital — and a polo match where none of it gets discussed directly, because everyone already knows.

Social Life Magazine has been operating inside that room for twenty-three years — five summer issues from Westhampton to Montauk, fall delivery to Upper East Side doorman buildings, 25,000 readers who are the demographic every luxury brand is trying to reach by doing things significantly less effective than simply being in the magazine. The brands here are not buying exposure. They are being introduced to people who have already decided to trust the publication that introduced them. If your brand belongs in that introduction: sociallifemagazine.com/contact.

The email list is the year-round version of the same room — 82,000 readers, same zip codes, the winter conversation. Free. Eleven seconds. Join it here.

Polo Hamptons is the event version of the same insight. There are gatherings people attend and gatherings where something actually happens — where the introduction that required six months of mutual adjacency becomes, on a July afternoon, simply a handshake between two people who were always going to meet. Category-exclusive sponsorships from $14,000. Private cabanas from $6,500. One sponsor per category. Most are already claimed. polohamptons.com.

The print subscription is the physical object on the coffee table in the house on Further Lane, handed by the family office principal to the person he is trying to introduce to the concept of your brand before the introduction has technically happened yet. Five summer issues. sociallifemagazine.com/subscription.

And then this, which is the most honest sentence here and therefore the one most likely to be skimmed: independent luxury media with no advertiser leverage and no engagement algorithm is genuinely rare, which is why the judgment, when present, is worth something. You have already formed an opinion about whether it was present here. If yes: paypal.com/donate. The amount is whatever you think that judgment is worth, which is the only honest way to price it.

Full profiles in this series:

Ken Griffin Net Worth: Citadel’s $49B Meadow Lane Titan

David Tepper Net Worth: The Revenge Mansion at $20B

George Soros Net Worth: The $40B Number Forbes Doesn’t Show

Leon Black Net Worth: Apollo’s $13B Shadow on Meadow Lane

Henry Kravis Net Worth: KKR’s $12B Meadow Lane Patriarch

Ronald Perelman Net Worth: The Creeks and a $19B Fall

Barry Rosenstein Net Worth: The $147M Further Lane Bet

Carl Icahn Net Worth: The $25B Raid and the $8 Stock

Hamptons hedge fund billionaires net worth data sourced from Bloomberg Billionaires Index, Forbes Real-Time Billionaires, and public company filings. Real estate figures from East Hampton and Southampton property records and public reporting. Social Life Magazine is an independent publication with no financial affiliation with any individual profiled in this series.

Author

Written by

Recent Posts

7 Mindful Meal Prep Tips for Stop Food Waste Day

Rebecca Ferguson Net Worth: The Advantage of Not Being the Lead

What Makes a Dinner Party Truly Unforgettable (Hint: It’s Not the Food)

Tips for Managing Grease and Oil in Everyday Dishwashing

Austin Butler Net Worth: The Method Actor in a Post-Method World

Categories

- Art

- Articles

- Beauty & Skincare

- Celebrities

- Celebrities|Entertainment

- Celebrities|Television

- Celebrities|The Chronicles

- celebrities|the-archive

- Chronicles

- Entertainment|Culture

- Event Photos

- Events

- Fashion

- Fashion & Style

- Featured

- Food & Beverage

- Food, Spirits, Wine

- Hamptons

- Hamptons Celebrities

- Hamptons Celebrities|Celebrities|The Chronicles

- Health

- Health & Beauty

- Lifestyle

- Luxury Lifestyle

- Movies

- Press

- Profiles

- Real Estate

- Technology

- The Chronicles

- Travel

- Uncategorized

- Weddings