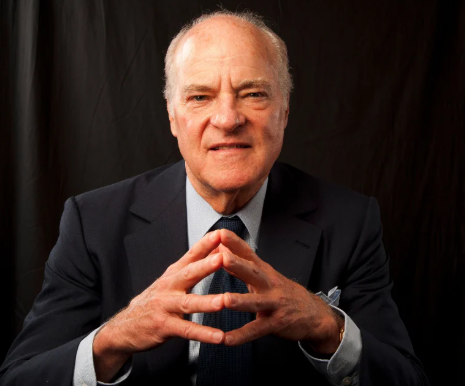

Henry Kravis net worth sits at approximately $12.5 billion as of early 2026. That fortune came almost entirely from one institution — co-founded with $10,000 of his own money in 1976. KKR — the firm he launched alongside his cousin George Roberts and their mentor Jerome Kohlberg — manages $744 billion in assets as of fiscal year 2025. The founding investment was $10,000. Notably, the return on that capital is not a figure the firm publicly calculates. It does not need to.

Meanwhile, his Meadow Lane compound in Southampton has been in the family for more than two decades. Indeed, that tenure is, by Hamptons standards, the clearest signal of all.

The Room Before the Room

Henry Roberts Kravis was born on January 6, 1944, in Tulsa, Oklahoma, into a family that understood how proximity to capital worked. His father, Raymond Kravis, was a successful oil and gas engineer whose clients included Joseph P. Kennedy — the patriarch whose own fortune was built on strategic positioning near power. That early education in how wealth moved through relationships and industries did not go unabsorbed. Kravis left Oklahoma for boarding school in Massachusetts at Eaglebrook, then Loomis Chaffee in Connecticut, where he was elected vice president of the student council. Subsequently, he attended Claremont McKenna College in California, majored in economics, played varsity golf for four years, and graduated in 1967. Furthermore, he completed his MBA at Columbia Business School in 1969.

Ultimately, his Wall Street career began at Bear Stearns. There, he joined his first cousin George Roberts and worked under Jerome Kohlberg in the corporate finance division. Together, the three began executing what they called “bootstrap investments” — buying family businesses too small to go public, whose founders needed an exit but had no obvious buyer. Consequently, the strategy was methodical, patient, and largely invisible to the broader financial press. Crucially, Bear Stearns executive Cy Lewis rejected every proposal the trio made to establish a dedicated in-house fund for the work. By 1976, after years of those rejections, Kravis, Roberts, and Kohlberg simply left — and built something bigger.

The First Day

On May 1, 1976, the three launched Kohlberg Kravis Roberts — the name had originally been planned as Kohlberg Roberts Kravis, but public relations advisors preferred the sound of KKR. Kohlberg contributed $100,000 in initial capital. Kravis and Roberts each put in $10,000. They raised their first fund piecemeal, with eight individual investors contributing $50,000 each.

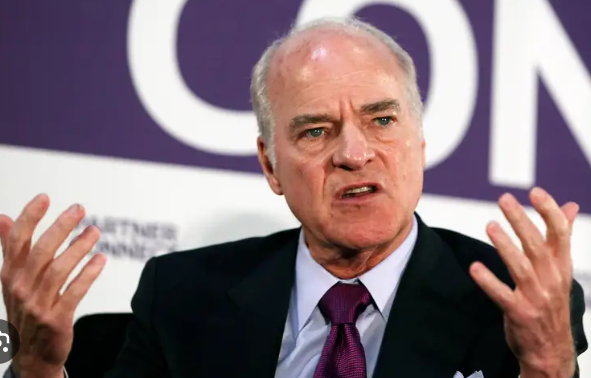

Decades later, at a Cornell lecture in April 2025, Kravis opened with his now-familiar line: “I didn’t have a clue what I was doing in 1976.” He said it to 1,300 students and investors. The room laughed. Ultimately, the point was always culture. The room laughed. The point was the culture. “On May 1, 1976, our first day as KKR,” he told them, “we spent more time discussing our values than our economics.” Their 20% carried interest model — now the standard across the entire private equity industry — was improvised on the spot, inspired by oil and gas partnerships they had observed growing up in Oklahoma.

The Belief System — The LBO as a Philosophy, Shown Through Two Deals

The leveraged buyout, as Kravis and Roberts practiced it, was not primarily a financial maneuver. It was a governance thesis: most public companies of the 1970s and 1980s were poorly run because nobody was accountable. Boards were passive. Management was entrenched. By acquiring a company with debt secured against its own future cash flows, KKR forced accountability. The debt had to be serviced. Performance became mandatory. Everyone running the business had to answer for results. Kravis articulated this directly at Cornell: “In the 1970s and ’80s, so many public companies were poorly run. Boards weren’t holding anyone accountable. We saw an opportunity to do better — to improve operations, not just finances.”

Two deals define the arc of that philosophy — one as triumph, one as instruction.

Duracell: The Clean Win

KKR’s acquisition and transformation of Duracell, the battery manufacturer, became the clearest proof of the LBO as an operational improvement vehicle, not merely a financial engineering play. Under KKR’s ownership, Duracell was rebuilt operationally and sold to Gillette in 1996 for approximately $7.5 billion — generating one of the most profitable exits in the firm’s history. The Duracell deal became a reference case for KKR’s LBO thesis: identify an underperforming asset, apply accountability and operational discipline, and return it to the market substantially stronger.

RJR Nabisco: The $31 Billion Education

In October 1988, RJR Nabisco CEO F. Ross Johnson announced a $17 billion management buyout of the company. Within weeks, KKR entered a counter-bid. The ensuing auction was frantic, public, and ferociously competitive. KKR won at $31.4 billion — then the highest price ever paid for a commercial enterprise. Journalists Bryan Burrough and John Helyar documented the deal in meticulous detail in Barbarians at the Gate, published in 1989 and subsequently adapted into a 1993 HBO film in which Kravis was portrayed by actor Jonathan Pryce.

By early 1995, KKR had divested its remaining RJR Nabisco holdings at an overall loss. Subsequently, the New York Times summarized it as a lesson in the perils of concentrating too much capital in a single transaction. KKR pledged never to commit such a proportion of a fund to one deal again. The deal that made KKR famous was ultimately the deal that cost it money. Kravis kept building anyway.

The Timeline: From $10K to $744 Billion

| Period | What Happened | Net Worth / AUM Marker |

|---|---|---|

| 1944–1969 | Born in Tulsa, Oklahoma. Father Raymond Kravis is oil engineer and business partner of Joseph Kennedy. Claremont McKenna economics degree (1967), Columbia Business School MBA (1969). | — |

| 1969–1976 | Joins Bear Stearns alongside cousin George Roberts, works under Jerome Kohlberg. The three execute early “bootstrap” LBOs: Stern Metals, Houdaille Industries, others. Bear Stearns exec Cy Lewis repeatedly blocks dedicated fund proposal. | — |

| 1976 | Kravis, Roberts, and Kohlberg leave Bear Stearns, found KKR. Kravis contributes $10,000 of personal capital — the only money he ever put in. Raises $30M+ first institutional fund in 1978 after ERISA revision. | AUM: $30M (1978 fund) |

| 1987 | Jerome Kohlberg resigns over strategic disagreements. Kravis and Roberts take full control. The firm pivots toward larger, more aggressive transactions. | AUM: growing rapidly |

| 1988–1995 | RJR Nabisco LBO: $31.4B, largest buyout in history at the time. Documented in Barbarians at the Gate. By 1995, KKR exits at a net loss. KKR vows never to over-concentrate a fund in a single deal again. | ~$1B+ personal est. |

| 1990s–2000s | KKR executes profitable takeovers: Duracell (sold to Gillette 1996), Safeway, Beatrice Foods, HCA Healthcare, TXU Energy. From 1976 to 1996, KKR funds return $33.8B in profits per SEC filings. | AUM: $50B+ by mid-2000s |

| 2007 | TXU Energy LBO: $45B, surpasses RJR Nabisco as largest buyout in history at the time. | AUM: $75B+ |

The Public Years: 2010–2026 |

||

The Public Years: 2010–2026 |

||

| 2010 | KKR lists on the New York Stock Exchange. From 1976 to June 2010, KKR funds have generated $43.8 billion in profit — a 91% total return. Kravis’s personal stake becomes publicly valued for the first time. | ~$5B personal (IPO est.) |

| 2017–2021 | Kravis and Roberts announce succession plan, naming Joseph Bae and Scott Nuttall co-presidents. In October 2021, the transition completes: both step down as co-CEOs, continue as co-executive chairmen. | AUM: $470B (2021) |

| 2022–2026 | KKR AUM reaches $744B (FY2025), up 17% year-over-year. Fee-Related Earnings hit $1B/quarter. AUM approaching $1 trillion. Kravis holds ~76M KKR shares. Personal net worth est. $12.5B (Bloomberg). Lawsuit filed alleging $650M+ in improper post-CEO share compensation (2024); KKR contests. | ~$12.5B personal; AUM $744B |

The Hamptons Chapter: Meadow Lane, Twenty Years In

Henry Kravis has owned his Meadow Lane compound for more than two decades — longer than any other property acquisition on his residential portfolio, and longer than most of his neighbors have held their addresses on the same strip. According to Hello! magazine’s recent survey of Billionaire Lane residents, the property is a six-bedroom, five-bathroom home on four acres of prime oceanfront land. That tenure — over 20 years on the same barrier strip between the Atlantic and Shinnecock Bay — is, in itself, a form of statement in a corridor where properties change hands for $40 million to $80 million and the arrival of a new neighbor generates press coverage.

Beyond Southampton, Kravis maintains residences in New York City, Palm Beach, Paris, and Sharon, Connecticut. Moreover, the geographic spread mirrors both the peripatetic life of a global capital allocator and the lifestyle architecture of someone who built an institution that operates in every major financial center on earth. Among the Hamptons power player cohort, Kravis is the senior figure in terms of continuous Meadow Lane tenure. Ken Griffin arrived in 2020. Leon Black has been there for years, but Kravis predates them both.

The Metropolitan Museum Connection

Kravis and his third wife, Marie-Josée Drouin — a Canadian economist — are among the most significant art patrons in New York institutional life. A wing at the Metropolitan Museum of Art bears their names: the Marie-Josée and Henry Kravis wing. Much of their collection adorns KKR’s Manhattan headquarters at 30 Hudson Yards. That combination — corporate headquarters as art gallery, Met wing as legacy infrastructure — reflects a mode of cultural patronage that positions the Kravis name inside the permanent architecture of the city rather than merely adjacent to it.

Henry Kravis Net Worth: What He Actually Built

Henry Kravis net worth, estimated at approximately $12.5 billion by Bloomberg as of 2025–2026, derives almost entirely from his KKR stake. According to a June 2025 Form 4 filing, Kravis holds approximately 76 million KKR shares directly and through affiliated entities, excluding shares held for charitable distribution. At KKR’s current valuation, those shares represent the primary engine of his wealth. From 1976 to 1996 alone, KKR funds returned $33.8 billion in profits per SEC filings. From 1976 to June 2010, total profits reached $43.8 billion — a 91% total return on invested capital across the firm’s entire history to that point.

Additionally, by fiscal year 2025, KKR’s total AUM had reached $744 billion — up 17% year-over-year — with Fee-Related Earnings hitting a milestone of $1 billion per quarter. The firm is approaching $1 trillion under management. According to Bloomberg’s Billionaires Index and Forbes, the KKR ownership stake drives his fortune. Real estate, art, and ancillary investments supplement it. For context: the $10,000 he invested in 1976 — his only personal capital contribution, ever — seeded a machine now managing more than sixty times the GDP of the country where he was born.

The Succession and What Remains

In October 2021, Kravis and Roberts stepped down as co-CEOs, handing daily operations to Joseph Bae and Scott Nuttall. Both founders continue as co-executive chairmen and remain active on KKR’s regional private equity investment committees. Furthermore, in August 2024, a lawsuit alleged that Kravis and Roberts received shares worth over $650 million tied to a tax receivable agreement. The suit claimed those shares benefited the founders without corresponding value creation for shareholders. KKR has contested the suit and sought dismissal. The case reflects a standard tension in founder-led firms: long-term equity arrangements versus post-succession scrutiny. Notably, it has not materially affected KKR’s performance or Kravis’s standing within the industry.

Public Reputation vs. What the Room Goes Quiet About

The established public narrative in finance: Henry Kravis invented the modern leveraged buyout. Together with Roberts and Kohlberg, he built a firm that redefined how capital could reshape underperforming businesses, built an institution that has executed over 770 private equity investments with approximately $790 billion in total enterprise value, and stewarded KKR through five decades of market cycles without a catastrophic failure. The Barbarians at the Gate deal that cost KKR money is consistently framed as a learning moment rather than a defining one, which is itself a measure of the firm’s subsequent record. An actor played Kravis in a major film. A wing of the Metropolitan Museum bears his name, and at 82 continues as co-executive chairman of a firm approaching $1 trillion under management. The approved narrative is formidable.

Inside finance, however, the room goes quiet about a different set of details. First, the RJR Nabisco loss is structurally underexamined. The deal that defined the LBO era in popular consciousness — the one with the book, the movie, and the business school curriculum — was a money loser. KKR subsequently pledged to never again concentrate such a proportion of a fund in a single transaction. That pledge is how you know the loss was serious. Second, there is Kravis’s political positioning. He contributed $1 million to Donald Trump’s 2017 presidential inauguration after years of supporting mainstream Republican candidates including George H.W. Bush, George W. Bush, and John McCain. That combination — centrist Republican donor turned Trump inaugural funder — sits uncomfortably in parts of the financial and cultural world Kravis inhabits simultaneously.

The Ownership Works Question

More recently, Kravis has championed an initiative called Ownership Works, designed to give frontline employees equity stakes in KKR portfolio companies. At his Cornell lecture, he described garage door factory workers walking away with $800,000 equity checks when their company was sold. The program represents either a genuine shift in how private equity thinks about labor — or a reputational hedge against decades of LBO criticism. Both readings remain available. That the program exists at all reflects the degree to which Kravis, at 82, is actively managing not just capital but legacy.

Contribution: To Whom, and at What Scale

Henry Kravis’s philanthropy follows the institutional naming-rights model more consistently than any other figure in this series. The Met wing is the signature. Beyond that, the Kravis Leadership Institute at Claremont McKenna College administers the Henry R. Kravis Prize in Nonprofit Leadership, established in 2006, which identifies and funds exceptional leaders in the nonprofit sector. Claremont McKenna and Marie-Josée and Henry Kravis administer the prize jointly. Additionally, Kravis has funded construction at Eaglebrook School, Loomis Chaffee, Middlesex School, and Deerfield Academy — the boarding school circuit he traveled as a teenager. In 2019, he received the Carnegie Medal of Philanthropy.

Notably, the pattern of giving is consistently educational and institutional. Kravis funds the places that shaped him and the places that produce the kind of leadership he values. Claremont McKenna gets the institute. The prep schools get buildings. The Met gets the wing. In fact, it is a geography of giving that traces the biography precisely: Tulsa origins, New England boarding schools, California college, New York cultural apex. The philanthropic map and the personal map are identical.

What the Record Doesn’t Capture

However, what remains less publicly documented is the scale of the Kravis family’s overall giving relative to net worth. Unlike Soros’s $32 billion in documented philanthropic transfers or Tepper’s $122 million to Carnegie Mellon, the Kravis giving record is harder to aggregate in a single number. The institutional footprint is visible — the Met wing, the Claremont institute, the prep school facilities — but the total dollar figure is not as clearly stated as the naming rights would suggest. Furthermore, the Ownership Works initiative, if it performs at scale across a significant portion of KKR’s portfolio, could ultimately represent the largest philanthropic output of Kravis’s career. It has not yet been measured in those terms.

The East End Verdict on Henry Kravis Net Worth

Henry Kravis net worth is the ledger of the man who, more than anyone alive, invented the financial instrument that restructured American corporate life after 1970. The LBO was not just a transaction type. It was a theory of accountability — the argument that debt-financed ownership forces performance in a way that passive public market shareholders never could. Whether that theory holds across the full LBO history — including deals that cost workers jobs and left companies over-leveraged — is a debate finance academics and labor economists have run for forty years. Kravis’s answer, delivered consistently, is that KKR’s record speaks for itself: $43.8 billion in profits generated by 2010, a firm approaching a trillion dollars under management, and portfolio companies where factory workers walk away with equity.

On Meadow Lane, he holds the longest continuous tenure of any current resident. That geography — the same four acres of Southampton oceanfront for more than two decades — is not an accident of real estate timing. It reflects the same quality that runs through the biography: patience, compounding, and the willingness to stay in a position long after others have moved on. Among the billionaires who summer on that strip, Kravis has been there longest. He built the institution that shaped the industry. He still shows up to Cornell lectures to say he had no idea what he was doing in 1976. The hedge fund geography of the Hamptons has no more fitting patriarch. Social Life Magazine has documented this coastline for 23 years — and on Meadow Lane, nobody has been here longer.

The Number That Matters Most

Ultimately, Henry Kravis net worth is not the $12.5 billion on the Bloomberg leaderboard. It is the $10,000 he put in at the beginning — the only capital he ever contributed personally — and the $744 billion that grew from it. Indeed, that ratio is, by any calculation in any field, one of the most significant return multiples in the history of American finance. The Meadow Lane address was not given. It was compounded, deal by deal, over fifty years, from an $10,000 check written in 1976 by a 32-year-old from Tulsa who had just been told no one last time at Bear Stearns. The Hamptons billionaire corridor is full of people who started with capital. Kravis started with a theory.

Want Social Life to tell your story? The people on this list were once unknown. Contact Social Life Magazine — we’ve been documenting Hamptons power for 23 years.

Meet the East End’s real decision-makers in person: Polo Hamptons — sponsorships, VIP cabanas, and brand activations where the Hamptons actually convenes.

The Hamptons insider list: Subscribe to Social Life Magazine — 23 years of the East End, delivered.

Support independent Hamptons journalism: Donate $5

Related Reading:

Ken Griffin Net Worth: Citadel’s $49B Meadow Lane Titan

Leon Black Net Worth: Apollo’s $13B Shadow on Meadow Lane

David Tepper Net Worth: The Revenge Mansion at $20B

George Soros Net Worth: The $40B Number Forbes Doesn’t Show

Hamptons Hedge Fund Billionaires: The Complete Net Worth Guide

Henry Kravis net worth data sourced from Bloomberg Billionaires Index and SEC Form 4 filings. KKR AUM figures from company earnings releases. Real estate details from public reporting. Social Life Magazine is an independent publication and has no affiliation with Henry Kravis or KKR.

Author

Written by

Recent Posts

7 Mindful Meal Prep Tips for Stop Food Waste Day

Rebecca Ferguson Net Worth: The Advantage of Not Being the Lead

What Makes a Dinner Party Truly Unforgettable (Hint: It’s Not the Food)

Tips for Managing Grease and Oil in Everyday Dishwashing

Austin Butler Net Worth: The Method Actor in a Post-Method World

Categories

- Art

- Articles

- Beauty & Skincare

- Celebrities

- Celebrities|Entertainment

- Celebrities|Television

- Celebrities|The Chronicles

- celebrities|the-archive

- Chronicles

- Entertainment|Culture

- Event Photos

- Events

- Fashion

- Fashion & Style

- Featured

- Food & Beverage

- Food, Spirits, Wine

- Hamptons

- Hamptons Celebrities

- Hamptons Celebrities|Celebrities|The Chronicles

- Health

- Health & Beauty

- Lifestyle

- Luxury Lifestyle

- Movies

- Press

- Profiles

- Real Estate

- Technology

- The Chronicles

- Travel

- Uncategorized

- Weddings