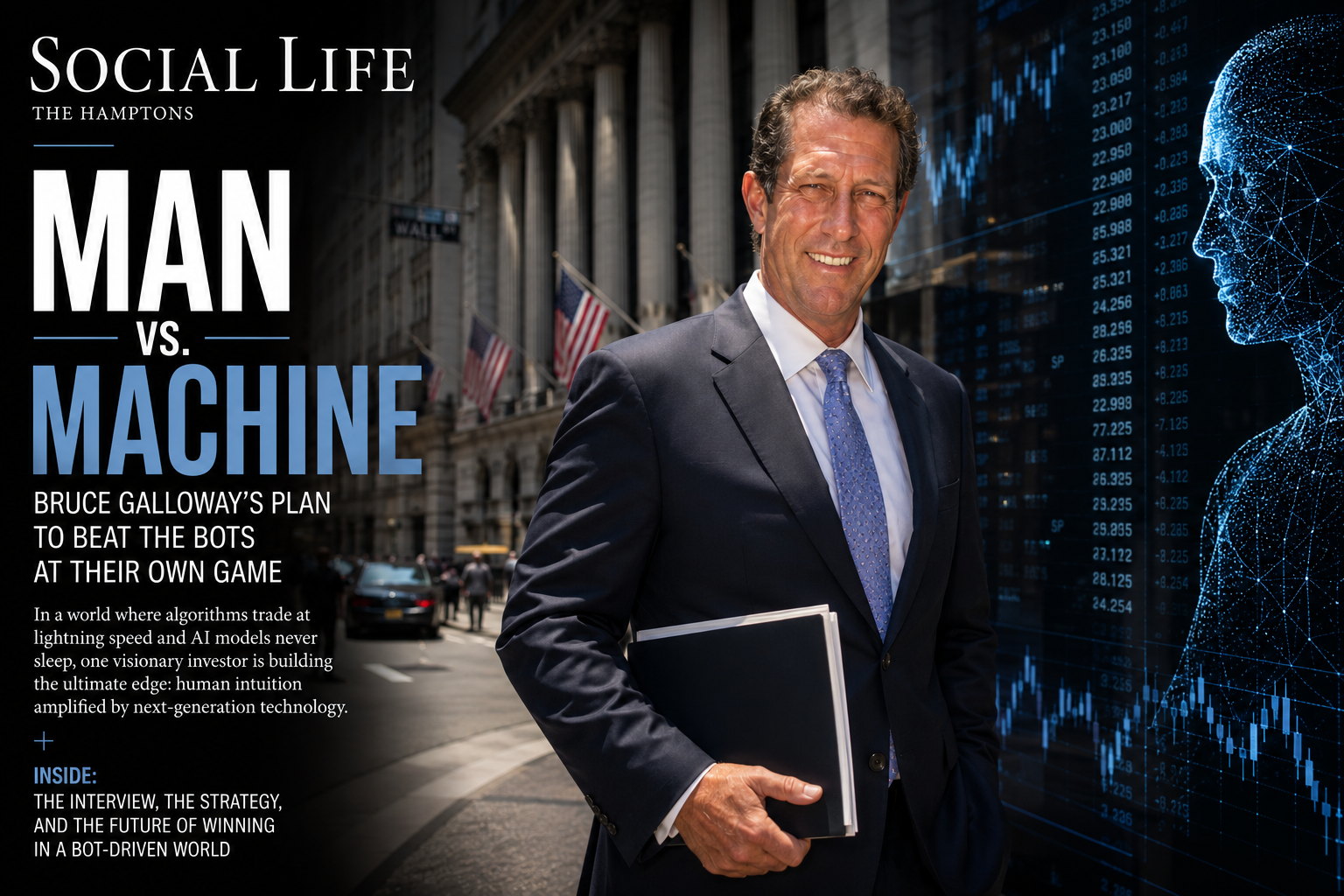

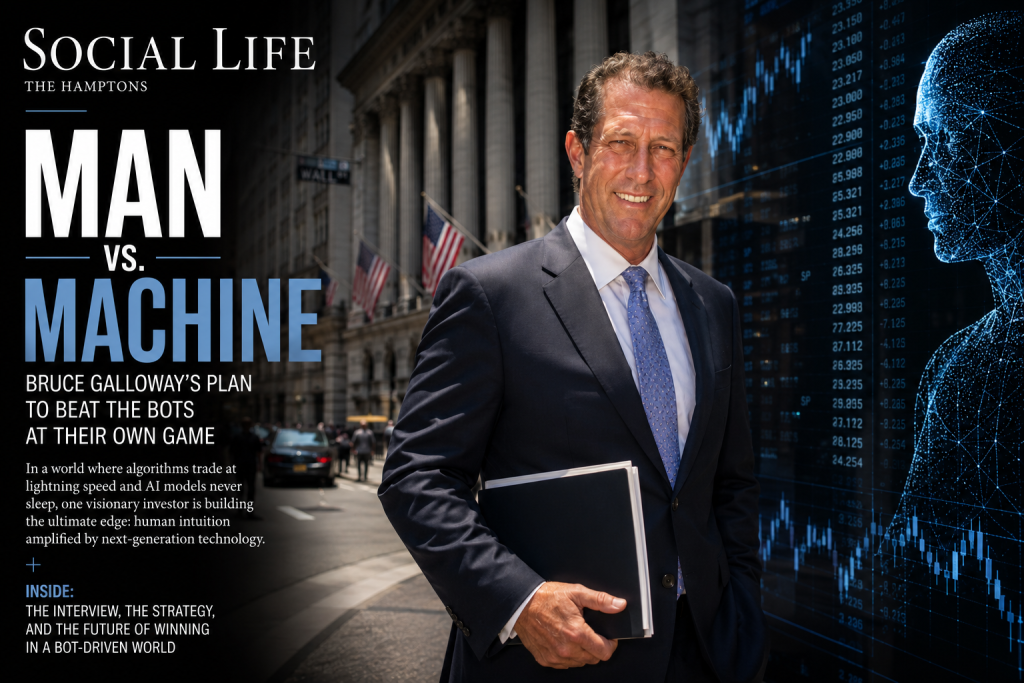

There is a moment in every fight when the smaller man figures out the bigger man’s rhythm. Bruce Galloway claims he found the market’s rhythm somewhere around 2018, and the discovery was insulting in its simplicity. The algorithms that now dominate trading do not think. In fact, they react, at scale, to the same signals, every time. So a seventy-something value investor in Miami Beach decided the machines were not opponents at all. They were a crowd that could be steered. As a result, his firm, Galloway Capital Partners, built an entire strategy on that premise and gave it a name that belongs on a fight poster. Man vs. Machine. This chapter of our five-era Wall Street series is the deep file on how the strategy actually works, trade by trade, filing by filing.

Who Is Bruce Galloway

The short version of the resume explains the long memory. Galloway started as a research analyst at Prudential after Hobart, added the NYU Stern MBA in 1983, and spent the Liar’s Poker years as a vice president at L.F. Rothschild. But that firm died in the 1987 crash, a formative funeral covered in our chapter on the 1980s. He then ran his own division at Burnham Securities for twelve years, founded Strategic Turnaround Equity Partners, and collected board seats the way other men collect watches. Five decades, every market regime, one discipline. Buy what is worth more than it costs, then make the market admit it. The biography matters here because the strategy is the biography. Only someone who watched humans set prices for thirty years could spot exactly where the machines set them wrong.

The Thesis: Why the Machines Broke the Market

Start with the most documented pattern in financial history. For roughly a century, value stocks outperformed growth stocks over time. Then, in the thirteen years after the financial crisis, the pattern inverted, and growth beat value by more than 300 percent. Of course, most explanations blamed interest rates or technology. Galloway’s explanation blames the buyers, because the buyers changed species. Algorithms, ETFs, and passive index flows came to dominate daily volume, and none of them read a balance sheet.

The consequences, after all, are mechanical. Index money buys whatever is already big, which makes the big bigger, which attracts more momentum code, which repeats. Meanwhile the same machinery systematically shorts small, cheap, profitable companies, because falling charts read as weakness to a program. The result is a feedback loop that prices popularity instead of value. The full anatomy of this rewiring fills the machine takeover chapter. The hub you are reading covers what one firm decided to do about it.

The Feedback Loop in One Trade

Picture a real company. It earns money, carries no debt, and trades at a fraction of book value. Yet no index holds it, no analyst covers it, and its chart slopes down. To the algorithms, that chart is the only fact that exists, so the shorting continues and the price detaches further from the business. In the old market, some human eventually noticed the gap and bought. In this market, the noticing function has been automated away. That orphaned gap between price and value is the entire opportunity set. Somebody simply has to walk in and close it.

The Counter-Strategy: Baiting the Bots

Here is the move that separates Galloway from the value investors who merely complained about the machines. He does not wait for the algorithms to come around. Instead, he studies what they respond to, then supplies it. The firm identifies what the programs are punishing, accumulates a position at the bottom of the code’s contempt, and introduces a catalyst the code cannot ignore. Volume spikes. Filing headlines. Insider buying signals. A sudden change in the momentum profile of a left-for-dead ticker. The same machines that crushed the stock on the way down flip, mechanically, into buyers on the way up. The bots never know they were used. Of course, that is the elegant part. You cannot offend software.

What the Algorithms Actually See

Knowing the audience matters, because the bots read a narrow menu of signals. Specifically, they watch volume, price momentum, short interest, options flow, and the machine-readable headline feeds that parse SEC filings in milliseconds. A 13D filing hits those feeds like a flare. So does a sudden volume spike in a ticker that has been dormant for years, or a string of insider purchases. None of these signals requires the code to understand the business, and that is precisely the exploit. A patient investor who controls the catalyst also controls, in effect, the moment the machines change their minds. The trade is no longer a bet on when the market will notice. It is a scheduled appointment.

The Catalyst Menu

Catalysts come in a few reliable flavors, and the firm screens for all of them. New management taking over a stale company. A recapitalization that repairs a frightening balance sheet. A regulatory change, a technology shift, or a turn in market sentiment that the code has not yet priced. Sometimes the catalyst already exists inside the company, waiting. Other times Galloway supplies it personally, which is where the activist toolkit enters. The screening process behind all of this, from the professional network to the solvency math, gets full treatment in our profile of the firm’s deep value operation.

The Execution Playbook

The activist sequence runs in three steps, and the first one is paperwork with teeth. Step one is the 13D filing, the public disclosure required after crossing five percent ownership, which announces to the market and the boardroom that an engaged shareholder has arrived. Our explainer on how a 13D filing works covers the mechanics. Step two is engagement, a specific list of actions delivered to management and the board. Step three, reserved for resistant boards, is the appeal to fellow shareholders, up to and including a proxy contest. The escalation ladder is climbed slowly and in public, because the audience for each step is partly the other shareholders and partly the algorithms watching the volume.

Friendly Activism’s Three Clocks

Galloway calls his style friendly activism, and the friendliness runs on three clocks. Initially, the short clock seeks asset sales, special dividends, and distributions, cash events that reprice a stock quickly. Then the middle clock works on board changes and management replacements, the slower surgery. Ultimately the long clock handles capital structure, buyback programs, and dividend policy, the compounding machinery. A target company can satisfy the short clock and buy itself peace. Still, the other two keep ticking, which is the polite menace at the heart of the method. The full history of how this style evolved sits in the activist decade chapter.

The Live Board

Theory is cheap, so look at the open positions. In May 2026 the firm disclosed an 8.42 percent stake in WW International, arguing that one of the most recognized wellness brands on earth should not trade below a $100 million market cap after cutting its debt by nearly a billion dollars. The GLP-1 era makes that bet stranger and more interesting, and our file on the WW International position unpacks it fully.

Noodles & Company is the other duel running in real time. Galloway disclosed 6.01 percent in December 2025 and pressed the chain to sell roughly 200 company-owned restaurants to retire expensive debt. By February 2026 the stake had grown to 8.78 percent and the tone had turned encouraging, because the company had executed a reverse stock split and the numbers were improving. Notably, the same deleveraging play revived Regis Corporation before this, and the precedent is the firm’s favorite proof.

The Babcock & Wilcox position shows the quieter version of the method. The firm announced a 4.31 percent stake in June 2025, just under the 13D threshold’s loudest setting, a holding pattern that keeps every option open while the energy infrastructure cycle does its work. Equally, positions in WidePoint, PodcastOne, and Trust Stamp spread the same thesis across cybersecurity, media, and identity technology. Babcock & Wilcox, Chegg, Heliogen, and the rest of the roster appear in the full 13D portfolio tour, and the firm’s fifteen anonymized future targets get their own treasure map in the special opportunities file.

Why Now: The AI Distortion

The next distortion is already arriving, and it is bigger than the last one. Artificial intelligence is flooding the market with fresh algorithmic buyers while simultaneously rewriting the fundamentals of entire industries. The code prices yesterday’s business models at today’s speeds. As a result, the gap between what a company is and what the machines think it is has rarely been wider, in both directions. Chegg is the perfect specimen, a company the market left for dead in the AI panic, now sitting in Galloway’s 13D portfolio as a contrarian wager on survival and repricing.

The anonymized target list tells the same story. A digital publishing company down from a $2 billion valuation to $100 million, holding $50 million in cash, positioned as an AI beneficiary. A pure-play AI infrastructure firm at a $390 million market cap that the major Wall Street desks have not bothered to cover. In particular, these are the kinds of mispricings that only exist because the noticing function broke. The sixth era of this story, whenever historians name it, will belong to whoever repaired it first.

The Risk Ledger

Honesty requires the other column, because deep value investing has a famous failure mode. Cheap stocks can stay cheap, and some deserve to. A catalyst can stall, a board can entrench, and a thinly traded small cap can punish anyone who needs to exit quickly. The firm’s answer is structural rather than heroic. Daily position monitoring, weekly portfolio reviews, statistical simulations, and Value at Risk analysis run constantly under the stock picking. Diversification rules cap every sector and position before conviction can become concentration. None of it eliminates risk. Still, it converts risk from a surprise into a line item, which is the most any investor can honestly claim.

The Scoreboard and the Asterisk

Performance claims deserve their sourcing, so here is both the number and the asterisk. By the firm’s own pro forma accounting, cumulative returns exceed 2,000 percent, with annualized returns above 50 percent, net of standard fees. Those figures are the house talking. The independent figure is louder anyway. In 2020, Eurekahedge ranked Galloway the number one value investor in the world, with returns of 164.44 percent that year, and sixth among all North American managers outside crypto. One number is a claim, and the other is a ranking with a referee. Together they explain why the Man vs. Machine thesis gets meetings instead of eye-rolls.

The Firm Behind the Fight

The operation stays deliberately small and deliberately boring, because restraint is the moat. Roughly forty to fifty positions. No single name above ten percent of assets, no sector above thirty-five percent, margin under twenty percent. Holding periods run one to three years, long enough for catalysts to detonate and gains to turn tax-friendly. Gary Herman, the co-founder, brings decades of turnaround structuring and a commercial pilot’s license, which suits a firm that flies into headwinds professionally. Russel Anmuth runs research with thirty years of special situations behind him. The trio’s full story sits in our profile of the team. The address is Miami Beach now, but the discipline is pure old New York.

Where The Conversation Continues

This hub anchors the modern era of our five-part Wall Street series, and the deeper files branch from here. Readers can trace the whole arc back through the fifty-year master map, or go straight to the live fights, the portfolio tour, and the anonymized targets. The print feature lands in our July issue, on coffee tables from Southampton to Montauk, exactly when the East End starts asking its favorite summer question. Who saw it first? In this story, the answer has been the same man for five eras running. The machines are still checking their code.