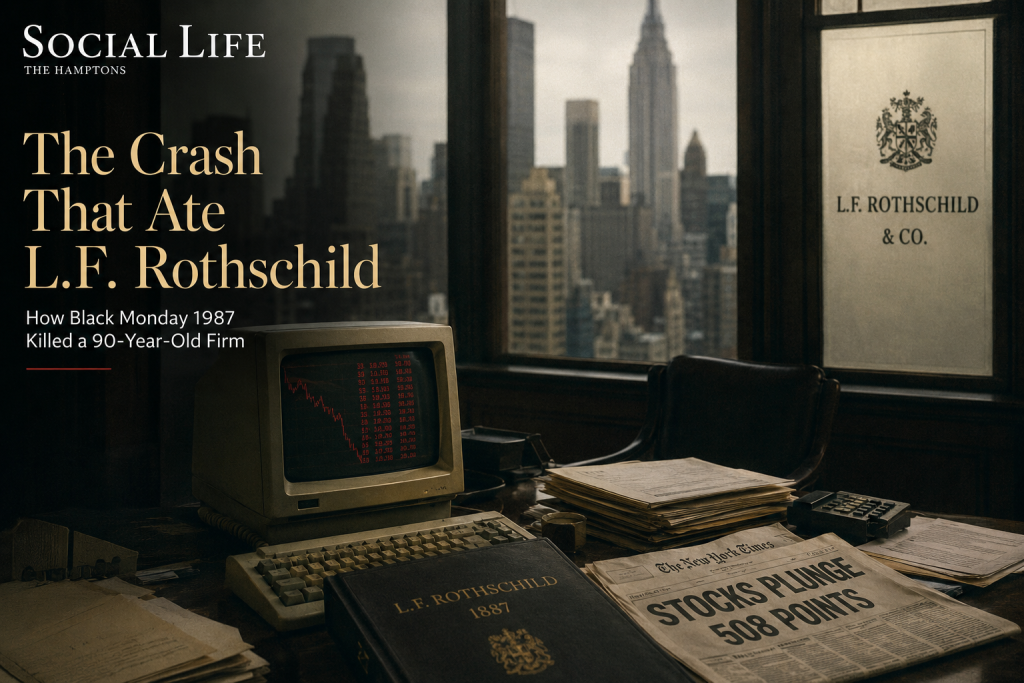

A firm can survive two world wars, the Great Depression, and ninety years of panics, then die in a single quarter. That is the story of L.F. Rothschild, and the story of Black Monday 1987 told through the one firm it killed outright. On October 19, 1987, the Dow Jones Industrial Average fell 22.6 percent in a single session, the worst one-day percentage decline in its history. Most firms absorbed the blow and recovered. Rothschild did not, and a young vice president named Bruce Galloway watched the collapse from inside, collecting the lesson that would anchor his next five decades. This file reconstructs that death completely, as part of our chapter on the Liar’s Poker decade. The crash was a market event. The funeral was a private one, and it taught more than the crash.

The Firm That Took Intel Public

Start with what was lost, because the loss was genuinely substantial. L.F. Rothschild was founded in 1899 by Louis F. Rothschild, unrelated to the European banking dynasty despite the borrowed grandeur of the name. The firm built a serious reputation across the twentieth century. By the early 1980s, in fact, it had become something remarkable. It was the leading underwriter of initial public offerings in America, surpassing the elite houses of the day. Among the companies Rothschild carried public were Intel, Cray Research, and Cetus Corporation, a biotech pioneer. Consider that roster for a moment. A single boutique bank introduced the semiconductor industry, supercomputing, and commercial biotech to public markets. Whatever happened later, this was not a marginal operation. It was, for a stretch, the most productive IPO machine on Wall Street.

The 1977 Merger

The firm’s modern shape came from a combination. In 1977, L.F. Rothschild merged with the boutique investment house C.E. Unterberg, Towbin, adopting the fuller name L.F. Rothschild, Unterberg, Towbin. As a result, the merger fused Rothschild’s established name with the entrepreneurial energy that would drive the IPO dominance of the early eighties. Notably, the combined firm specialized in emerging-growth companies. These were the technology and biotech names that the bulge-bracket banks initially overlooked. For most of a decade, then, the strategy worked brilliantly. The firm rode the new-issue boom to the top of the league tables. Then the founders left, and the timing of their departure would prove fateful in ways nobody could have scripted.

The Cracks Before the Crash

The firm was already straining well before October. In 1986, Thomas Unterberg and A. Robert Towbin, two of the three names on the door, left to join Shearson Lehman. Publicly, the split was attributed to a strategic disagreement, since the two opposed management’s plans to expand the firm’s bond sales and trading operations. According to insiders, the deeper story involved a capital-raising negotiation in which an attractive outside offer required the pair to step down. Hard feelings followed and drove them out. That detail matters enormously in hindsight. The founders who opposed expanding the trading operations left, the expansion proceeded, and precisely that trading exposure would destroy the firm one year later. Sometimes the people who leave a company are the ones who read its risks most clearly.

Public at the Wrong Moment

In March 1986, the firm’s stock debuted at $20.50 per share, converting the old partnership into a public company with permanent capital and public shareholders. The move was fashionable, since the eighties had taught Wall Street that permanent capital meant safety and scale. Yet the logic contained a fatal flaw. Public ownership meant the firm now carried its trading losses on a visible balance sheet, marked to a market that could panic. After all, a private partnership absorbs a bad quarter quietly. By contrast, a public firm watches its solvency get repriced in real time by the same crashing market that caused the losses. Rothschild had traded the partnership’s discretion for the public company’s exposure, eighteen months before the exposure became lethal.

The IPO King’s Vulnerability

The firm’s great strength concealed its great weakness, as strengths often do. An IPO machine built on emerging-growth technology and biotech names depended entirely on a receptive new-issue market. When investors felt optimistic, the pipeline flowed and the fees poured in. Yet that same business model collapsed the instant sentiment turned, because nobody floats a speculative growth company into a crashing market. So Rothschild carried a double exposure into October 1987. Its trading desk would take direct crash losses, and its core underwriting business would freeze simultaneously. The two engines that had powered the firm’s rise were wired to fail together. Diversification, the oldest protection in finance, was exactly what this specialized house lacked. Brilliance in one cycle had become fragility for the next.

October 19, 1987

Then the Monday arrived without warning. The crash of October 19, 1987, descended with a violence that still has no equal. No single day since has matched it. The Dow lost 508 points, 22.6 percent of its value, in one session. Unlike later crashes tied to clear catastrophes, this one arrived from within the market’s own machinery. Automated portfolio insurance programs amplified it, as explored in our chapter on the decade. For firms heavily exposed to equity trading and market-making, therefore, the day was not a setback but an extinction-level event. Rothschild had expanded exactly into that trading exposure, over its founders’ objections. It sat directly in the blast radius. The market would recover within two years. The firm would not have two years. It barely had two quarters.

The Anatomy of the Losses

The numbers tell the death plainly enough. Rothschild suffered roughly $56 million in arbitrage and over-the-counter trading losses tied to Black Monday, with immediate hits exceeding $35 million in equity capital. For the fourth quarter of 1987, the firm posted a net loss of $128.8 million. Total revenue that quarter was just $32.5 million. Read those two figures together, since their relationship is the whole story. A firm cannot lose four dollars for every dollar of revenue and survive. Not when its capital is finite and its losses are public. The market-making and arbitrage operations that had been expanded for growth became, in a single afternoon, the channel through which the firm’s capital drained away. The expansion the founders opposed did precisely what they feared, only faster and worse.

The Long Dying

In practice, death came in stages across two years. By the months after October, the firm had already cut about 1,000 jobs, leaving 1,200. It sold off retail branches and withdrew from public finance and municipal bond trading entirely. Then a rescuer appeared in 1988, when Kansas-based Franklin Savings Association acquired the firm and pumped $30 million in new capital into it. Still, the infusion bought time, not survival. Rothschild’s stock had debuted at $20.50 in 1986. By then it traded around $3, a decline of roughly 85 percent that priced the outcome accurately. Even with Franklin’s capital, the holding company filed for Chapter 11 bankruptcy protection in July 1989. By the end of that year, L.F. Rothschild had collapsed from a peak of 2,200 employees to 45. A ninety-year institution had become a skeleton crew, and then a memory.

What Killed It, Precisely

The cause of death deserves precision, because the precision itself is the lesson. Rothschild did not die from a bad year, a fraud, or a failure of strategy in the ordinary sense. It died from the interaction of three choices with one bad day. The firm expanded its trading exposure, then went public to fund that expansion. Those moves placed its now-visible capital directly in the path of a market crash. Of course, none of those choices looked reckless in 1986, when every fashionable theory endorsed scale, permanent capital, and trading revenue. The crash revealed them as a single concentrated bet against catastrophe, and catastrophe arrived on schedule. The firm’s age, its pedigree, and its glorious IPO history provided exactly zero protection. Markets do not grade on tenure.

Why Some Firms Lived

The instructive comparison is with the firms that survived the same Monday. The bulge-bracket houses took enormous losses too, yet most absorbed them and continued, because their size, diversification, and private or deep-pocketed capital structures gave them shock absorbers Rothschild lacked. A firm with trading losses offset by stable advisory fees, asset management, and a fortress balance sheet could bleed and live. Rothschild, specialized and freshly public, had converted itself into a pure bet on the new-issue cycle precisely when that cycle was about to stop. The lesson generalizes cleanly. Survival is an architecture, not an outcome. The firms that lived had built the capacity to be wrong, while Rothschild had optimized that capacity away in pursuit of growth. One design assumes bad days arrive. The other assumes they never will.

The Investigations After

The collapse left regulatory wreckage as well. The probes that followed examined how Rothschild had managed its trading risks and capital requirements, and they highlighted systemic vulnerabilities in over-the-counter and small-cap market-making. Those findings contributed to broader reforms in market oversight and risk controls after 1987. The pattern is familiar across this series. A disaster exposes the gap between how a business claimed to manage risk and how it actually did, and regulators rebuild the rules around the lesson. Each era in our story has its version of this reckoning, from the 1980s market-making probes to the post-2008 banking overhaul. The reforms rarely prevent the next crisis. Instead, they ensure the next one arrives wearing a costume the old rules cannot recognize.

The Lesson Galloway Kept

Bruce Galloway held a vice presidency at L.F. Rothschild during these years, practicing the research craft inside a firm everyone assumed would outlive them all. Watching it die, however, rearranged his understanding of risk permanently. The lesson was not subtle, and it became the foundation of everything afterward. Price and value are different animals, and only one of them can kill you. A firm, like a stock, can carry a magnificent past and a fatal present at once. The past offers no defense. Every discipline his own firm now publishes traces directly to this funeral. The limited borrowing, the position caps, the obsession with surviving the bad day rather than maximizing the good one. The complete framework appears in our profile of Galloway Capital Partners. Deep value discipline, in the end, is Black Monday converted into a permanent process.

The First Machine Crash

One more lesson hides in the wreckage, and it echoes through the entire series. Black Monday was substantially a machine crash, the first of its kind, accelerated by automated programs that all sold together faster than human judgment could interrupt. The same dynamic, rebuilt at a thousand times the scale, would define the algorithmic market three decades later. That story is the subject of our chapter on the machine takeover. An investor who watched portfolio insurance turn a decline into a collapse in 1987 was unusually prepared. He understood early what algorithms would later do to price discovery. The Rothschild funeral, in other words, was also an education in machine behavior. Galloway attended both lessons in a single October, and filed them both.

Where The Conversation Continues

The death of L.F. Rothschild is the human cost behind a statistic everyone knows, and it sits at the center of our five-era story because the survivor carried it forward for fifty years. The wider decade fills the Liar’s Poker chapter, and the full arc runs from the fifty-year pillar. Our print feature lands in the July issue, Out East, where more than one summer fortune was either made or nearly unmade on that October Monday. The survivors tell the story differently than the textbooks do. They remember it as the day that taught them what tenure is worth in a market, which is nothing, and what discipline is worth, which is everything.

Author

Written by

Recent Posts

The Activist Education: Board Seats, 13Ds, and the Decade That Built Friendly Activism

The Hamptons Village Hierarchy, Ranked by the People Who Live It

The Noodles & Company Campaign: A Friendly Activist Fight in Real Time

Inside Galloway Capital Partners: The Deep Value Machine, Documented

New Money vs Old Money: The Hamptons Status Divide Nobody Explains